")

While most GCC markets are similar in terms of their oil-based economies and their limited natural resources that would support and stimulate significant international leisure travel, some destinations are just different. Unlike the obvious development of the hospitality sector in the GCC over the last five to seven years, with many cities leading this growth and attracting substantial local and foreign direct investments and a high number of travelers, Oman’s tourism development strategy has focused primarily on enhancing the tourism infrastructure. This has included roads, the airport, local training and employment within the hospitality industry, and a well-defined strategy for marketing and promoting the country. Oman enjoys a stable political, economic and social system and boasts unrivaled natural resources as well as a rich culture.

There are eight main governates in the sultanate — the main governates being Muscat, Dhofar and Musandam. The climate varies from one area to another. There has been noticeable growth in demand for hotel accommodation across Oman in the last couple of years, largely due to the government’s marketing and promotional campaign, the increase in visitor numbers to the Middle East as a whole and Oman’s set of unique conditions that make it an attractive tourism destination.

The direct contribution of travel and tourism GDP

The tourism industry made a direct contribution of an estimated OMR 1.34 billion to the economy in 2019, accounting for 4 percent of GDP. The contribution of tourism to GDP has grown annually at a CAGR of 5 percent between 2015 and 2019. Investment in travel and tourism increased by 8 percent annually from 2015 to 2019, reaching OMR 35O million in 2019. It is expected that there will be further government spending post Covid-19 to revivify the industry.

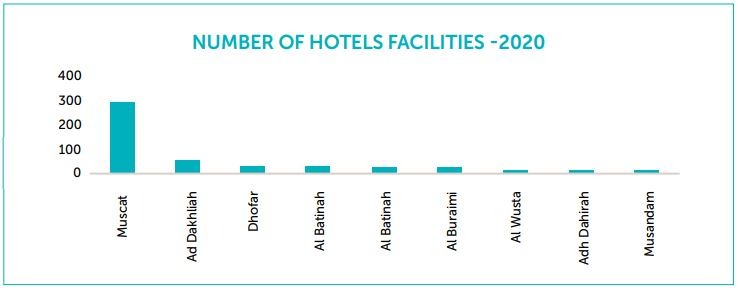

Existing supply in 2020

In September 2020, there were 512 branded and non-branded properties in Oman. Five-star hotels, which accounted for 28 percent of the total, dominated the branded hospitality market, while 21 percent fell in the midscale and four-star category and the remaining 51 percent were locally managed, unclassified properties. With 298 hotel establishments, Muscat had the largest hotel stock in Oman. The market is forecast to have an additional 11,000 keys by 2025. As per Vision 2040, Oman is expected to have an additional 50,000 keys by 2040 compared to 2015.

Oman Tourism Strategy

Vision 2040 aims to increase tourism’s contribution to GDP to 10 percent, create 535,000 jobs in the tourism sector, welcome 11 million international and local tourists and achieve 14 million room nights. A critical element of the Oman Tourism Strategy is the planned system of clusters. Each cluster comprises well-serviced groups of attractions and features ample accommodation, a transportation network, tourist facilities and services.

Airport arrivals — Muscat

• Between 2010 and 2019, arrivals at Muscat International Airport grew by 170 percent from 5.5 million to 14.9 million passengers.

• Muscat, Salalah and Sohar international airports experienced a drop of around 70 percent in international arrivals compared to YTD October 2019. The trend reflected those witnessed at major airports in the region and around the world in 2020.

Source markets — Muscat

The Muscat market comprises domestic travelers (52 percent), Europeans (25 percent), Asians (7 percent) and GCC nationals (5 percent). Other countries and other Arab source markets have played a minor role in tourism demand, contributing 5 percent and 3 percent respectively to the total number of hotel guests. The European market continues to deliver the highest number of international visitors to Muscat as the government increases its marketing efforts in these countries.

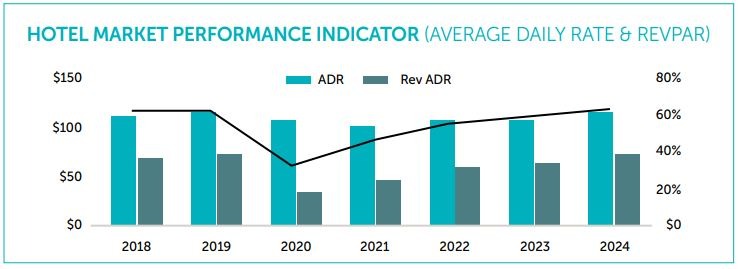

Hotel market performance — Muscat

Over the past decade, average hotel occupancy in Muscat stood at 60 percent, compared to Dubai (70 percent), Bahrain (52 percent), Doha (61 percent) and Jeddah (71 percent). In 2019, occupancy in Muscat was registered at 61 percent, while the GCC average was 65 percent. Gradual recovery of the hotel market in Muscat is forecast between 2021 and 2023, and the hotel market is expected to stabilize in 2024. Over the last two years, Muscat’s hotels benefited from unexpected demand from travelers on the way to and from Doha as a result of the Qatar diplomatic crisis, which sparked travel restrictions between Doha and several other countries in the region.

What to expect

Historically, the hotel market was characterized by a local pool of investors. However, we anticipate an increased level of regional investor appetite in the medium term. We expect that many financing (and refinancing) transactions for proposed and existing hotels in the market may also take place in this period. Furthermore, we consider that investment opportunities exist in various segments of this market, notably in: wellness resorts, desert resorts and branded limited service hotels.

Hala Matar Choufany

President

HVS Middle East, Africa and South Asia